Debunking Myths About SBA Financing

SBA financing can be a great solution for real estate brokers working with clients looking to purchase commercial real estate for their business to occupy. This financing can be a fit and in many cases offers the most competitive rate and terms.

Key Advantages of SBA 504 Financing

Lower Down Payment: Get up to 90% financing, keeping more cash in your business

Flexible Approvals: Suitable for deals that traditional financing might not approve

Competitive Rates: Provides fixed, competitive interest rates

Predictable Payments: Enjoy set monthly payments for better cash flow management

Fully Amortizing Term: No balloon payments—pay off the loan over its full term

However, you may be thinking about the downside of SBA loans you’ve heard in the past or had an experience where you relied on SBA financing to come through just to experience delays and have these threaten the real estate contract. The SBA has seen some great improvements over the past several years, so let’s set the record straight.

Myths About SBA Financing

Myth: The application process is overwhelming.

Reality: The SBA application process has been greatly simplified. There is a single SBA 504 application form and it is generally completed by the majority business owner on behalf of all owners. The required documentation - such as the project details and financials - is generally in-line with what’s needed on a non-SBA, conventional loan request, making the process far less intimidating than many assume.Myth: SBA underwriting is cumbersome.

Reality: Recent reforms have reduced and simplified the underwriting process. For example, SBA lenders no longer have to collect financials and fully analyze each related business entity an owner has ownership in or collect spousal, non-owner signatures on personal financial statements. These changes save time and reduce complexity.Myth: SBA loans are slow and unreliable.

Reality: The SBA’s current average turnaround time is just over three business days. With the right Certified Development Company (CDC) and lending partner, a SBA 504 loan can be approved and closed within 30 days of application, for projects purchasing existing real estate without renovations. Projects with construction or renovation can also move very quickly and are initially funded under a bank’s or credit union’s permanent and interim loans.Myth: There’s a risk of surprises during approval.

Reality: Working with experienced SBA lending partners can help avoid any surprises. Clear and transparent communication is key to ensure the borrower and lending partners are on the same page. In addition, having a CDC partner that is clearing applications early on through SBA’s compliance framework can help ensure a smooth approval process.

Now that we’re on the same page on the benefits and new streamlining of the SBA program, how do you know if the property you’ve listed for sale or your client is looking to buy is a good fit for the program? To determine if SBA 504 financing is the right choice, here are some key eligibility criteria and deal details:

SBA 504 Deal Structure: Is Your Project a Fit?

Eligible Businesses:

For-profit businesses located in the United States.

Tangible net worth less than $20 million and after-tax profit less than $6.5 million.

The business will occupy at least 51% of the property (60% for new construction).

All owners with 20% or more ownership will agree to a personal guarantee.

A demonstrated credit need, typically due to needing a higher loan-to-value financing structure or a longer term than conventional financing allows.

The SBA 504 program is designed to support active, operating businesses, not passive enterprises. Many businesses are eligible for SBA financing including some industries that many find surprising such as hospitality, self storage, car washes and liquor stores. In addition, some of the business types that are the most active include restaurants, professional services (physicians, dentists, attorneys), child care and auto repair.

Some examples of ineligible businesses include speculative construction companies, real estate leasing enterprises and businesses involved in the marijuana industry.

What’s the structure of a SBA 504 loan:

The SBA 504 loan program can provide up to 90% financing for businesses looking to buy, build or renovate owner-occupied commercial real estate; purchase machinery or equipment; or refinance loans used for these purposes. Professional fees, bank fees and closing costs can be included in the financing as well.

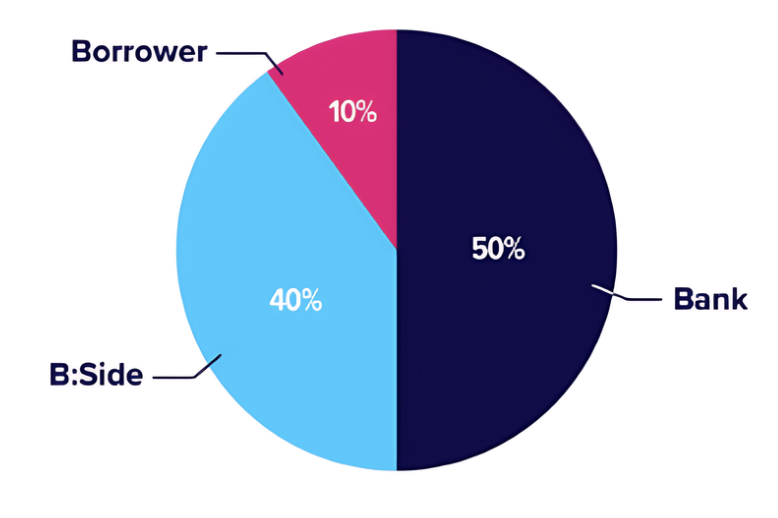

Typical Equity Structure:

Generally the bank or credit union provides 50% of the total project cost, and B:Side Capital on behalf of SBA provides up to 40% of financing. The borrower comes in with a minimum of 10% equity. If the business has less than two years of borrowing history or if the subject commercial property is considered limited/special purpose - an additional 5% borrower equity is required. If both apply, an additional 10% or total 20% of equity is needed.

Questions? Contact us!